The short answer? The lease should specifically address whether taxes are reconciled as part of operating expenses or are reconciled separately. But, why should this matter?

This week, we were working on an office tower acquisition in the southeast. The majority of the leases had the typical “tenant pays a proportionate share in excess of the base year” language. Both Operating Expenses and Real Estate Taxes (both capitalized) were defined very well by the leases. However, this was a situation where the leases were poorly written and rather than addressing a year end reconciliation of Operating Expenses as well as a year end reconciliation of Rea Estate Taxes, the leases addressed a reconciliation of Operating Expenses and Real Estate Taxes – so addressed only one time instead of two separate times.

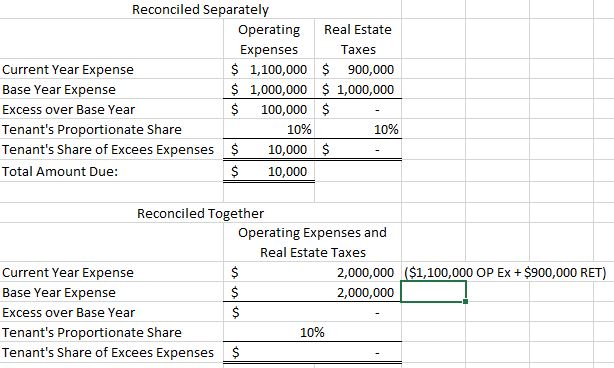

The leases read, “The tenant will pay its proportionate share of current year Operating Expenses and Real Estate Taxes over Base Year Operating Expenses and Real Estate Taxes.” What made the scenario critical was that current year Operating Expenses were much higher than Base Year Operating Expenses, while current year Real Estate Taxes were much lower than Base Year Real Estate Taxes. Reconcile separately, the landlord bills excess for Operating Expenses and gets nothing for Real Estate Taxes. Reconcile together and the landlord leaves money on the table.

Take the following simple example:

- Tenant’s proportionate share – 10%

- Base Year Operating Expenses – $1,000,000

- Base Year Real Estate Taxes – $1,000,000

- Current Year Operating Expenses – $1,100,000

- Current Year Real Estate Taxes – $900,000

As you can see, there can be a real difference between reconciling together or separately. In the case of the acquisition, considering this scenario affected a number of tenants and has a material impact on cash flow, our client has requested that the seller obtain letter agreements from the tenants clarifying that the charges are reconciled separately. If the seller fails to obtain the letter agreements, cash flow for purposes of the purchase price will be reduced to reflect a combined reconciliation rather than two separate reconciliations.

Another example of somewhat innocuous lease language affecting the cash flow and value of a property.