As a landlord, we talk about triple net all of the time. Often, our goal is to have our net cash flow be as close as possible to total minimum rent as possible. In order to do that, we want to get as close to 100% recoveries on reimbursable expenses – CAM, tax and insurance – as possible. However, as landlords, we should all intuitively know where our absorption is going to come from – which tenants, or types of tenants, or categories of spaces that will cause shortfalls. If we identify those areas, we can keep our leakage to a minimum – as much as the leases will allow now, and, through changing our leases by attrition, even lower in the future.

In our last blog, we took a look at an aerial and addressed the types of issues we see that will impact the property’s reimbursables. Today’s blog will look at a lease plan/site plan to identify some of the issues that will impact our ability to recover 100% of expenses.

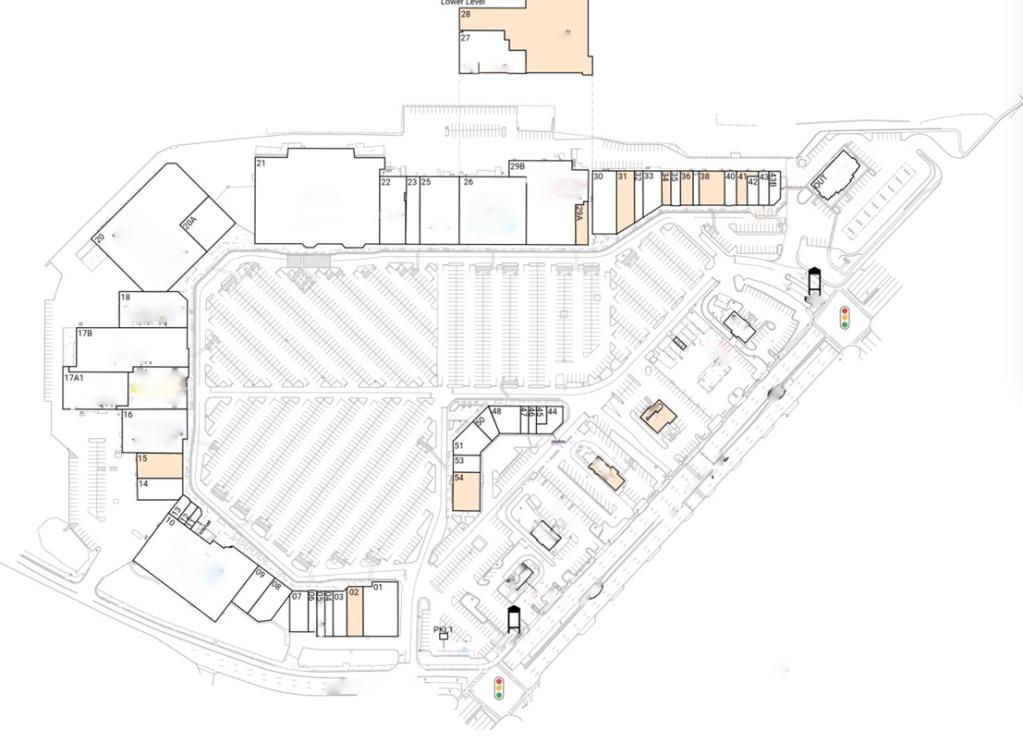

So, when you look at this particular site plan, what do you see? As I did with the aerial, I will go through and put some of mine, but, please, add your own insights.

- The two lowest hanging issues are fairly easy to spot – vacancy and the lower level area.

- Vacancy – This particular center is about 450k sf. Ballparking, we have about 50k sf of vacancy. Even if every tenant in the center paid a full prorata share based upon leasable, we are starting with the likelihood of > 10% leakage (50/450 = ~11%). So, going into the center, I am hoping we’ll have at least some of the leases on “leased” rather than leasable. If every remaining tenant was on “leased” (which would never happen), we’d be back to 100% collection (because we’d use a denominator of 400k instead of 450k).

- Lower Level Space – In retail, if there is any square footage above or below the ground floor, they are much less likely to be paying a full prorata share – with the reasoning that they are not getting the same benefit of full access to the common areas.

- This particular lower level space does have access to a rear parking lot. Despite this, it is not a primary parking area and is accessed by driving behind the center (I did look, the space canalso be accessed by a stairwell from the front. But, again, not primary).

Recognizing this issue, we would go in hoping to see one of two approaches:

- Leases defining lower level space as excluded, or, better yet,

- Leases defining the denominator as ground floor area

Why is that “better yet”? In the case of defining the lower level as an excluded area, it calls attention to the fact that it is being excluded. By using, “the denominator shall be the ground floor area of the center…,” the lower level is automatically excluded. (This is useful for centers with upper levels as well.)

Moving on from the two more obvious issues, we have:

- Numerous big boxes and outparcels that:

- Likely pay less than a full prorata share

- Likely exclude certain expenses

- May be self maintaining

- May be self insuring

- May be controlling the lighting in their critical areas

- May be separately assessed

Any one, or a combination of more than one, will cause absorption. Again, we go in hoping we get to exclude these tenants. If so, we will reduce our leakage.

One thing that is often not considered in ground leases/outlots is that the premises is often defined as the land itself. Therefore, if a tenant is required to provide not only all risk on its premises, but liability as well, the liability insurance may be required to be on the entire parcel. It is common for a landlord to be thinking that certain tenants may self-insure for all risk. But there is a possibility that we have to exclude for liability as well.

- Take a look at this portion of the center:

- There are a few issues going on here. One of those spaces is definitely “non-fronting” on the main parking areas. Like the lower level, we expect them to pay less than a full prorata share, and we are hoping they are a defined excluded area.

- Less obvious, we would go in to this property thinking that this group of tenants was once a big box that had been subdivided because a landlord would not typically intentionally create a non-fronting space at the initial development. (Likewise, I’d lay odds that if we went back decades, the lower level space was likely a basement area for some sort of department store. Again, it was likely not intentionally initially created that way.) But, why would this subdivision be notable? Because we would look for leases that defined excluded areas as “the buildings marked as excluded on exhibit…” In that case, the original building may have been marked as an excluded area, and that group of tenants would still be considered excluded.

- There are numerous other issues to be considered here – outparcels that may be on separate parcels (are they part of the center as defined, or excluded from the center to begin with; do their taxes and square footage get included, or must they be excluded?) Likely outparcels the landlord does not own that have ingress and egress through the center (and should, therefore, be making contributions).

As was the case last week, these issues may or may not exist at this center. But, by analyzing the aerial in advance, we can adjust our plan of attack for an acquisition of property lease audit. And, through attrition, we can adjust the leases to improve our cash flow going forward.

In the next post, we’ll address some of the issues you can glean from a Google street view walk around a center. I hope you are starting to see that your back office and some attention to detail can improve your cash flow!!!